Welcome back to another series of Battle of the Challenger banks!

We are thrilled to be back and starting on another series of Battle of the Challenger banks. We were so excited with your response the first time so we thought it would be fitting to embark on another journey. This time, however, our ‘battleground’ is not Europe, but the USA. That’s right! You read correctly. We are flying over the big pond to the USA.

Just like last time, every third Thursday of the month we will be releasing a new episode, exploring different user journeys for our contenders from their iOS channel.

But why Challengers again?

Well, Challengers banks have been increasingly taking larger and larger shares of the USA digital banking market. Due to their digital first nature, they have continued to grow exponentially in customer popularity, offering more and more digital offerings through their digital channels.

Especially during the pandemic they showed high preparation in catering customers who were unable to reach bank branches. Several of them have seen immense growth of up to 40% in users 2020. Challengers are considered the unicorns of the fintech ecosystem and have been for years the heralds of innovation in the digital banking industry.

Why start with KYC?

First of all, because of nostalgia! This is how we started it the first time around so it wouldn’t make sense to not continue like so. Secondly, it would be remiss of us not to select digital onboarding as the topic of comparison of the first episode as it represents the very first user journey prospective users experience. It is for most customers the first point of contact with a Challenger. The emphasis of KYC should be on providing an experience that will be memorable, smooth and above all convenient.

Of course the only way we would be able to carry on these battles is by using  . The digital banking research platform analyzes and UX-evaluates all features and their user journeys from banks and fintechs worldwide across all channels.

. The digital banking research platform analyzes and UX-evaluates all features and their user journeys from banks and fintechs worldwide across all channels.

For this episode we have extracted data about the KYC processes of US Challenger banks for their iOS channels.

Ready to start?

But first, let's meet our US contenders.

The Contenders

A pretty hefty list. Let’s see how they stack against each other! Here are all the steps that each challenger has included in their iOS channel KYC process in some pretty infographics.

Challengers go!

US Challengers KYC

What impressed us?

- Acorns customers have to answer a series of 7 questions to set up their investment account during the process of opening a bank account. This includes questions about their employment, income, net worth, investment goals, level of finance education, the amount they plan to invest and the level of control over them. This allows for a very thorough understanding of what customers really want the account for.

- Aspiration users are able to enroll in ‘Plant Your Change’ a wonderful initiative through which they can support reforestation. They can also choose the fees they’d wish to pay for their banking and 10% will be donated to a charity.

- Daylight as an LGBTQ+ bank allows users to specify the pronouns they wish to be addressed with. This is extremely important as it will avoid assumptions about gender and will factor in actual preference. LGBTQ+ customers will no longer have to receive wrongly-addressed responses and communication.

- Envel informs their new customers immediately about the length of their KYC process with a helpful progress bar at the top of the screen. Customers this way know if they have the time to complete the whole process rather than discover later that it might be too long and drop out.

- SoFi offers their customers the unique feature of choosing to open a joint account with another user during the KYC process. This is extremely useful to customers who want to open such an account and have to do so after the KYC and following another process. It saves time and effort of going through a second process when this can be done immediately.

- Stash new customers are not only able to open a new account and build their investment profile with their KYC but are treated to investment lessons as well. They can opt in to educate themselves on the basics of investing through Investments 101.

- In Revolut, Aspiration and N26 ID details can be input through a photo. Customers can take a photo of their ID card or passport and the details will be recognized and automatically filled in the relevant fields. This saves users time typing in their details.

What causes customer friction?

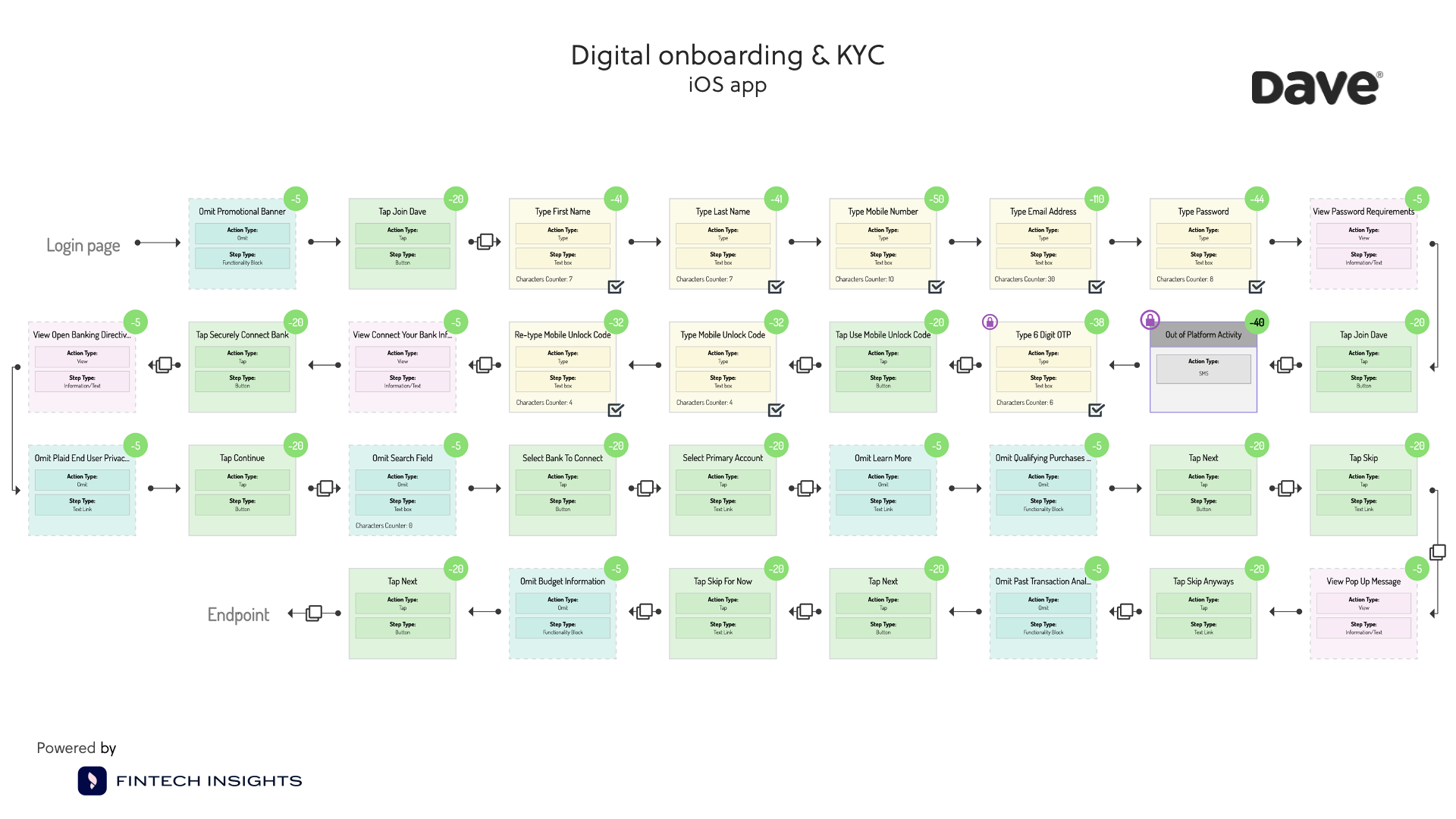

- Dave’s user journey is at times boggled with various promotional ads for the Challenger’s products. While we are always excited to see more of the bear mascot, having many ads can be great friction to customers who just want to open a digital account for the first time.

- MoneyLion requires their customers to contact their support team in order to set up a PIN and activate their virtual card. Having to call to activate the card is inconvenient for customers as the process is ultimately not completed fully online. New customers don't want to have to wait for a representative to help them when they apply online. If they wanted to talk with a representative they could've visited a bank branch or selected phone banking.

- N26 customers have to navigate between the web browser, their email for verification and the app multiple times during the KYC process which can be quite frustrating and confusing for them.

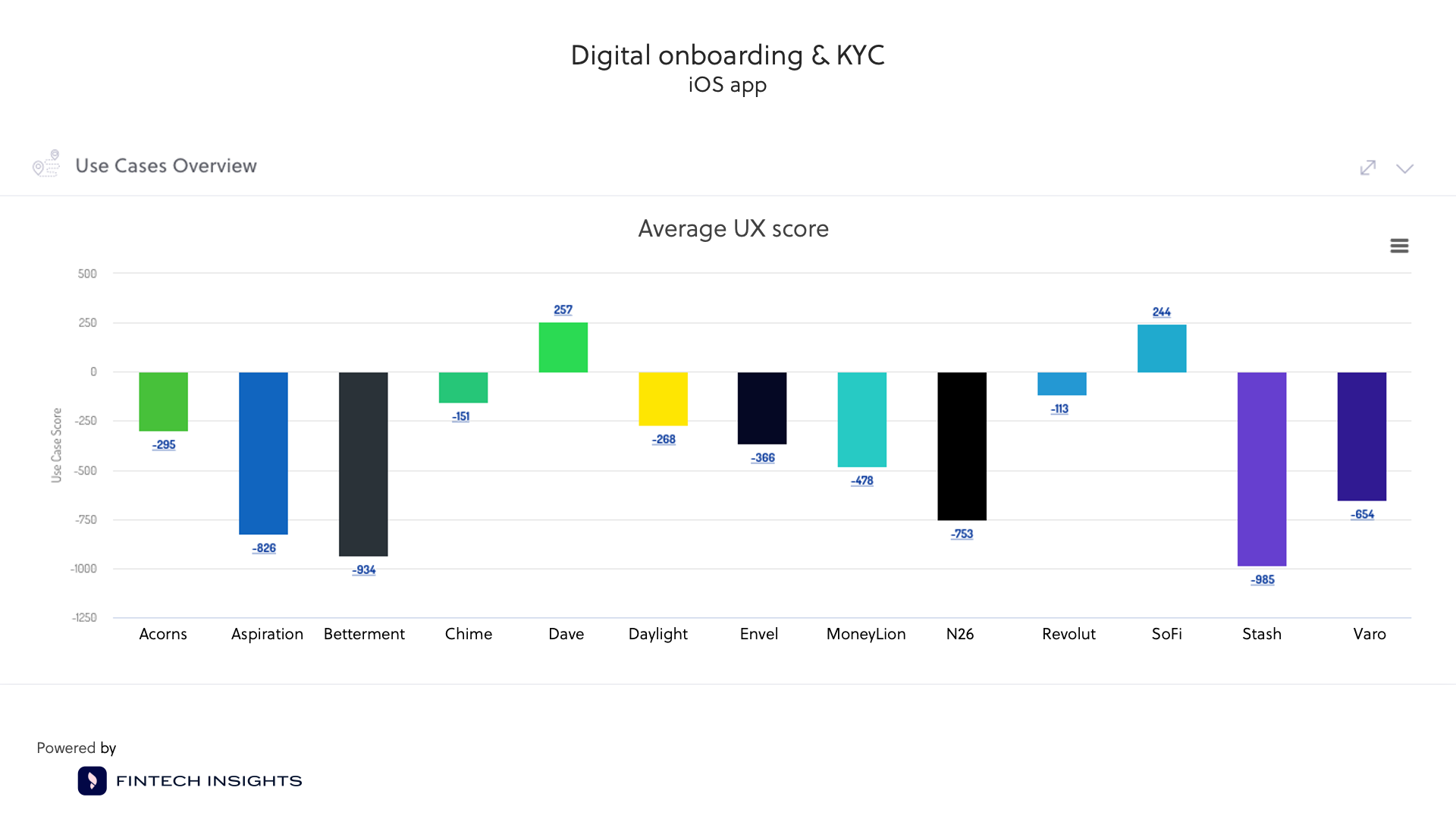

Which Challenger banks have the best and worst KYC experience?

Now that we have had a look at each of their individual KYCs, it's time to crown our winner. After all this is a battle!

The winner of our first US Battle of the Challengers is…

Dave and SoFi!

.gif?width=480&name=giphy%20(6).gif)

We have a double crowning!

Both Dave and SoFi offer customers the opportunity to open a digital banking account in a smooth KYC process that takes less than 35 steps (steps can be passive like reading information or active like typing). This may seem like a lot of steps but we have to take into consideration the regulation involved in the US.

Their user journeys are evaluated at 257 for Dave and 244 for SoFi out of 1000 according to Scientia’s Perfect 1000 UX scoring system. The two Challengers provide a seamless experience to new customers who get to know them for the first time. At a time when studies show that simplicity and speed are customer necessities and conjure up a convenient experience, these Challengers created journeys that are quick and easy.

Not everyone, however, provides equally smooth KYC processes for their customers. According to our data from , Stash’s digital onboarding process ranks as the least UX-friendly for customers with -985. It takes 104 steps to complete the process and open the account mainly due to the fact that the customer is also building their investment profile. It does, though, run the risk of customers dropping out midway through the process as it can be very tiring to complete a lengthy KYC. This is highly inconvenient for new customers as they also receive no indication from the bank of the length or progress of the application throughout Stash’s KYC.

That’s all folks… at least for this episode of US Battle of the Challengers.

SoFi and Dave were the clear winners of round 1. But there are several more rounds to got till we have the ultimate winner.

The battles are back and better than ever, so stay tuned for episode 2 next month.

Hint: we will be getting new cards in the mail.

Hungry for more?

Check out these episodes of the previous Battle of the Challengers in the Europe:

Help me build towards my wealth

Explore